What is Bookkeeping? You probably must have heard this from somewhere, or probably was taught to you during your high school days. Well, it is basically the Systematic recording and organizing of financial transactions in a company.

Bookkeeping has to do with the day-to-day recording of financial transactions and information that has to do with business. It ensures that records of the individual financial transactions remain correct, up to date, and comprehensive. So, accuracy is very essential to this process.

Bookkeeping offers details from which accounts are prepared. This step is quite distinct, and it takes place with the broader scope of accounting. Each of the sales doesn’t matter if it is a sale or purchase, it must be recorded. Structures are usually set in place for bookkeeping that is called ‘quality controls’, and this helps to ensure accurate and timely records.

Bookkeeping tasks

Essentially, what bookkeeping means is recording and keeping track of the numbers that are involved in the financial side of the business in a more organized way. It is very important for business but is also for individual and non-profit organizations.

The person placed in charge of bookkeeping for a business is required to take a record of all the transactions that are related, including but not limited to:

- Expense payments to their suppliers

- Loan payments

- Customer payments for invoices

- Generating financial reports

- Monitoring asset depreciation

The bookkeeping and accounting terms are usually identical, but accounting holds the entire practice when it comes to financing management either by individual or business, while bookkeeping refers to the tasks and practices that are involved in recording the financial activities.

Methods of Bookkeeping

Right before you start doing bookkeeping, you are expected to choose the method that you want to follow. When choosing, you are expected to consider the volume of daily transactions that your business has and the amount of revenue you get to earn. If your business is a small one, complex bookkeeping methods created for enterprises might cause some unnecessary complications. Bookkeeping methods include:

Single-entry Bookkeeping

This method is one straightforward method where one entry is made for all the transactions found on your books. Each of these transactions is found in a cash book just to track revenue and outgoing expenses. You are not required to have formal account training when it comes to the Single-entry system.

The small entry was created to suit all small private companies and sole proprietorships that are not buying or selling on credit, Own little to no physical assets, and hold a small amount of inventory.

Double-entry Bookkeeping

When it comes to double-entry we are talking about some more robust. This method follows the principle that every transaction affects a minimum of two accounts, and they get recorded as debits and credits. Let’s say you make a sale of $10 and your sales account would be credited by the same amount. In this double-entry system, the entire credits are expected to always be equal to the total debits. When this occurs, your books are “balanced.”

This method is much better when used in a large business, in public, or buys and sells on credit. Enterprises usually select the double-entry system because it leaves less room for error. In a way, it ‘double-checks’ your books based on the fact that each transaction would be recorded as two matching but offsetting accounts.

Cash-Based or Accrual-Based

Selecting between cash or accrual basis the nest bookkeeping. This decision depends on when your business gets recognized its revenue and expenses.

In a cash-based, you get to recognize the revenue when you receive cash into your business. Expenses would get recognized when they are not paid for. each time cash enters or leaves, it would be recognized in the books. What this means is that every purchase or sale made on credit would be heading straight into your books until the cash exchanges.

In the accrual method, the revenue gets recognized when earned. Similarly, the expenses get recorded when they are finally incurred, usually along with corresponding revenues. The actual cash does not get to enter or even exit for the transaction to get recorded. You would be able to mark your sales and purchases that you made on credit immediately.

Cash and accrual basis work with both the single or double-entry bookkeeping.

How to Record Entries in Bookkeeping

Generating Financial Statements just like balance sheets, income statements, and cash flow statements would help you to understand where your business stands and gauge its performance. In other for the reports to show your business accurately, you are expected to properly document records of your transactions. the methods include:

Cash Registers

This device is an electronic machine that is used when calculating and registering transactions. cash registers are usually used to record cash flow in stores. The cashier collects the cash for a sale and then brings back the balance amount to the customers.

The journal

This is a book that is called the original entry. It is where businesses chronologically record their transactions for the very first time. When it comes to a journal, it can be digital or physical (in form of a book). The date of each transaction, the accounts credited or debited, and the amount involved. While the journal is usually not checked for the balance at the end of the fiscal year, each of the journal entries would affect the ledger.

The ledger

This is a book or accounts that is compiled together. It is also called a book of the second entry. After you enter the transactions in a journal, they get classified into separate accounts and then transferred into the ledger. These records get transcribed by accounts in the order of Assets, liabilities, equity, income, and expenses. Just like the journal, the ledger also can be physical or can be an electronic spreadsheet.

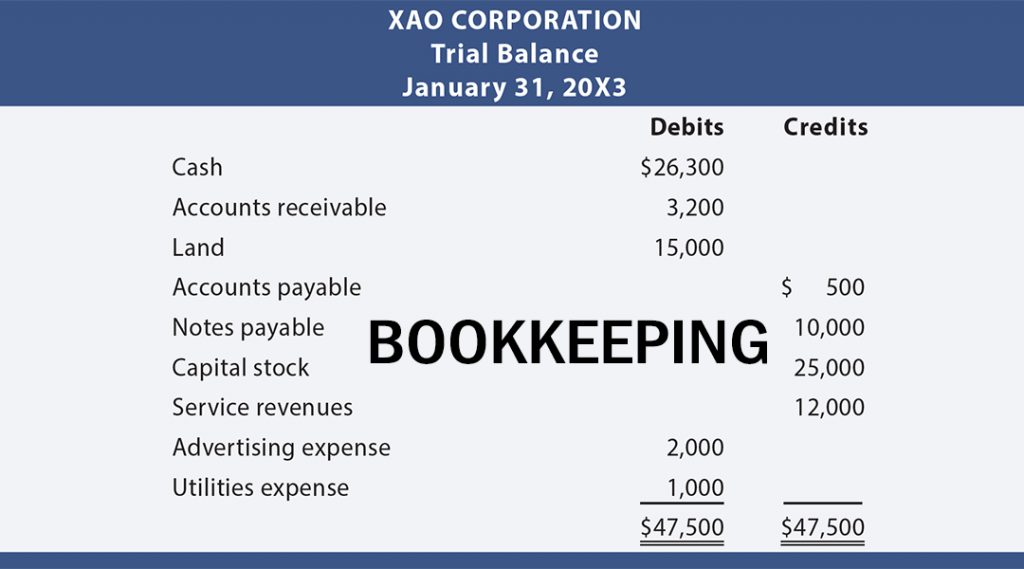

Trial balance

This is produced from the compiled and summarized ledger entries. The trial balance is more like a test to find out if your books are balanced. It lists the accounts exactly in the following order: assets, liabilities, equity, income, and expenses with the ending account balance.

You May Like This;

{kind=link}